Forging industry in-depth report: forging, from "iron horse" to high-end equipment era "Jingo"

Time:

2024-07-23

1. Forging process: the divider of the historical era, the former of the golden iron horse

1.1 forging process has a long history

Forging process has a long history, promoting human civilization into the "Iron Age". The manufacturing ability of human tools promotes the progress of history, and the utensils and production processes promote the development of human history.

The "three-phase theory" of human history: in 1836, Christian Yuensen Thomson put forward the "three-phase theory". According to the materials of human tools, human history is divided into three periods, namely, the "Stone Age", "Bronze Age" and "Iron Age". Although pottery has been widely used, but as a container is not the main production tool, failed to independently "lead" an era, but the pottery process to promote the development of metallurgy, casting, forging and other manufacturing processes.

The application of stone tools, bronzes and pottery lays the conditions for the forging process and the application of iron.

The excavation of raw materials during the use of stone tools promotes the discovery of metals. According to archaeological discoveries, about 2.5 million years ago, the first human beings appeared in East Africa. One of the major characteristics is that they began to make and use stone tools, and human beings also entered the Paleolithic Age. As early as about 10000 BC, humans began to make and use grinding stone tools, and entered the Neolithic Age.

In the process of quarrying, man found pure metal. Because gold, silver, and copper have relatively inert chemical properties, they were first discovered and used by humans. Around 9000 BC, humans began to forge sterling silver and pure copper. The early forging products were mainly small decorations. Later, with the increase of pure metal, they also began to forge some tools, mainly pure copper. But at that time, stone tools were still the dominant production tools, and the amount of pure metal tools forged was very small. In any case, the activity of forging natural metals has enriched human understanding of metals.

The emergence of pottery kilns provided high temperature and reducing atmosphere, which promoted the development of metallurgical industry. The development of the pottery industry paved the way for forging. As early as the Paleolithic Age, in addition to polishing stone tools as tools, human beings also developed another skill-pottery making. The pottery kiln produced with pottery manufacturing could reach a high temperature of more than 900 degrees Celsius as early as 6000 BC, and provided a CO reducing atmosphere. The combustion mass used by human beings in the early days is mainly wood. In the environment of insufficient oxygen, the gaseous CO produced by the high temperature combustion of wood can reduce the red iron oxide (Fe2O3) in the clay to black iron oxide (Fe3O4). The discovery of metallurgy is a long process. It took 5000 or 6000 years for humans to use stone tools to make jewelry to extract the first pure copper.

Drilling technology broadens the channels of metal collection. The ancients developed the technology of sinking wells for the need of drinking water. As stone, ore is generally stored in stony mountains and underground rocks, and drilling technology has given human underground mining capabilities; the development of metallurgical technology has also greatly improved human enthusiasm for prospecting up and down the mountain.

The advantages of 1.2 forging are obvious, conforming to the requirements of equipment for lightweight and high strength.

Wrought iron has higher strength, stronger toughness and more economy, and promotes mankind to enter the iron age.

The strength and toughness of wrought iron are higher than that of bronze, which is more suitable for the manufacture of cold weapons. The toughness and ductility of iron itself is higher than that of copper, and the strength of its material can be enhanced by repeatedly forging iron blocks at high temperatures. Under the same strength, the toughness of iron is far better than that of bronze. The cold weapons of the Bronze Age were mostly made into stabbing daggers, while the cold weapons of the Iron Age became popular for chopping knives. In addition, the forging process requires high ductility and toughness of the metal. As the main material for forging, the discovery and large-scale use of iron have also promoted the development of the forging process.

The relative abundance of iron in the crust is higher than that of copper, which is more economical. The abundance of iron in the crust is greater than that of tin and copper, and the cost is relatively low. Due to the high cost of copper itself, bronze was mainly used for ritual vessels and weapons in the Bronze Age, and could not completely replace stone tools as the main production tools. Because of the economy, the iron completely replaced the stone tool as the main production tool, which promoted the development of the forging process.

Metal forming process classification: casting, plastic forming, machining, welding, powder metallurgy, metal injection molding, metal semi-solid forming, 3D printing and so on. Among them, the history of casting and forging is the longest and the most widely used.

Compared with casting and machining, forging has advantages in terms of part integrity, texture streamline, and part flexibility.

Plastic forming optimizes metal properties by changing the metal microstructure. After plastic deformation, metal materials not only change the shape and size, but also have a series of changes in the internal structure and performance. The microstructure of metal materials will change obviously. In addition to a large number of slip bands and twin bands, the grain transfer will also change, that is, each grain will be elongated or flattened along the direction of deformation, and the internal structure of the metal will change, thus optimizing the performance of the metal.

Forging also provides structural integrity unmatched by other metalworking processes. The main raw materials for forging are metal bars, ingots, etc. These raw materials in its smelting, pouring and crystallization process, will inevitably produce pores, shrinkage and dendritic crystals and other defects, therefore, the casting process is difficult to produce competent to withstand the impact or alternating stress of the working environment parts (such as transmission spindle, ring gear, connecting rod, rail wheel, etc.). Forging eliminates internal voids and air pockets that can weaken metal parts. Forging provides excellent chemical homogeneity by dispersing segregation of alloys or non-metals. Predictable structural integrity reduces part inspection requirements, simplifies heat treatment and machining, and ensures optimal part performance under field load conditions.

The grain characteristics of the forging determine the directional toughness of the forging. By mechanically deforming the heated metal under severe conditions, forging can refine the coarse grains, resulting in a dense metal structure, which in turn results in predictable grain size and flow characteristics. In actual operation, by pre-processing the forgings, the dendritic structure of the ingot can be improved and the pores can be eliminated, and the mechanical properties of the forgings can be improved. This quality translates into superior metallurgical and mechanical qualities and better directional toughness in the final part.

Forged parts have the best metal texture flow lines. Forging is a processing method that makes the billet or ingot produce partial or complete plastic deformation under the action of pressure equipment and workers (dies) to obtain parts (or blanks) with certain geometric dimensions and shapes and to improve their organization and performance. After forging, the metal material has good shape and dimensional stability, uniform structure, reasonable fiber structure and the best comprehensive mechanical properties.

2. Open a broad axe to build heavy equipment, the necessary heavy equipment for big country competition.

2.1 forging is a must for soldiers in the industrial age.

A number of modern theoretical foundations laid the foundation for forging technology, and the discovery and proposal of Pascal's principle in 1653 promoted the development and iteration of human forging equipment. Forging technology is based on the principle of plastic forming, metalology, tribology as the theoretical basis, and involves heat transfer, physical chemistry, mechanical kinematics and other related disciplines, with a variety of technology, such as forging technology, together with other disciplines to support the machine manufacturing industry.

The discovery of Pascal's principle pushed open the door to large forging equipment. In 1653, French physicist Pascal discovered that after any point in the incompressible still fluid is subjected to pressure increase by external force, the pressure increase is transmitted to all points in the still fluid in an instantaneous time. Based on this, he proposed Pascal's principle. Using this principle, two pistons can be connected in the same fluid system. By applying a small thrust to the small piston and transmitting the pressure in the fluid, a larger thrust will be generated in the large piston. Pascal's principle was also used in the hydraulic press, which laid the foundation for the invention of the hydraulic forging machine.

The United States was the first to manufacture more than 10,000 tons of forging equipment, and large-scale forging equipment has attracted much attention from manufacturing powers such as the United States, the Soviet Union, Germany, France, and Czechoslovakia.

In 1893, Bethlehem Steel Company of the United States produced the world's first 10,000-ton free forging hydraulic press, and Sue and Germany immediately followed suit. At the beginning of the 20th century, with the development of heavy machinery and equipment, the tonnage of hydraulic presses increased rapidly. In 1905, the first oil-based hydraulic press with oil as the working medium was further improved. In 1934, the former Soviet Union built the first 10000-ton hydraulic press at the New Kramatorsk Heavy Machinery Plant (N M). In the same year, Germany successfully developed a 7000-ton die forging hydraulic press. Since then, Germany has successively manufactured one 30000-ton die forging hydraulic press and three 15000-ton die forging hydraulic presses before 1944.

After the end of World War II, the great powers competed to develop large die forging presses.

After the end of World War II in 1945, the United States and the Soviet Union began to realize the importance of large die forging presses. They removed four die forging hydraulic presses from Germany, two 15000-ton die forging hydraulic presses from the United States, and one die forging hydraulic press from the former Soviet Union for 15000-ton and 30000-ton die forging hydraulic presses. These equipment has also become the technical basis for the manufacture of ultra-large die forging presses in the United States and the Soviet Union. In 1947, the Kuomintang government also took back five 1000- 3000-ton hydraulic presses from Japan on the grounds of war compensation. These hydraulic presses were used as "trophies" and later became the starting point for the development of forging equipment in New China.

After the end of World War II, forging equipment in various countries developed rapidly. In 1950, the United States began to implement the "Air Force Heavy Press Program" (The Air F r e e vy Press Pr gr m) and decided to build two of the world's largest 45000-ton and two 31500-ton die forging presses funded by the federal government. In 1955, the United States Mesta (MESTA) heavy machinery plantAmerican Aluminum(a) One 45000 ton die forging press and one 31500 ton die forging press were constructed. In the same year, the United States (LOEWY) Company also built a 45000-ton die forging press and a 31500-ton die forging press for Wym n-G rd n. These four large die forging presses laid a solid foundation for the United States to dominate the world aviation industry.

At this time, Czechoslovakia still existed in the form of a republic and had not yet disintegrated into two independent countries. In 1956, they successfully put into operation a 12000-ton die forging hydraulic press in the S ODA plant. Later, during the Great Leap Forward, in order to promote the development of heavy industry, a 12000-ton free forging hydraulic press was imported from Czechoslovakia and installed in the Deyang Second Heavy Machinery Factory, which was still under construction at that time.

The former Soviet Union vigorously promoted the development of the forging industry for the development of the aviation industry.

From 1957 to 1964, in order to develop the aerospace industry, the former Soviet Union successively built six die forging hydraulic presses of more than 10,000 tons, including two 75000-ton die forging hydraulic presses, three 30000-ton die forging hydraulic presses and one 15000-ton die forging hydraulic press, the main builders of these six units are the New Kramato Heavy Machinery Plant (M3), the Ural Heavy Machinery Plant (Y3TM) and the Novosibirsk Heavy Machinery Plant.

Among them, the New Kramato Heavy Machinery Factory (M3) built two of the world's largest 75000-ton die forging hydraulic presses for the former Soviet Union, which were installed in the Gubyshev Aluminum Factory and the Upper Salda Titanium Factory respectively. The two largest giant machines in the world at that time were 34.7 meters high, 13.6 meters long and 13.3 meters wide. Their foundation was 21.9 meters deep underground and their total weight was 20500 tons. The size of the worktable is 16 meters × 3.5 meters, and it is driven by 12 cylinders and 8 columns. The net height of the mold space is 4.5 meters and the slider stroke is 2000mm. They are the national treasure equipment of the former Soviet Union's aviation industry system, which was inherited by Russia after the collapse of the former Soviet Union in 1991. The plant is now Russia's largest manufacturer of titanium alloy products-the Upper Salda Metallurgical Production Union (VSMPO-AVISMA).

France missed forging development opportunities, the development of aviation manufacturing industry was affected, must purchase forging press or forging parts from other countries.

In 1953, France built two 20000-ton die forging hydraulic presses in Aesop Company and Cr ut-L respectively to manufacture aviation aluminum alloy forgings, but there has been no large die forging press exceeding 40000 tons. In 1976, France's Aubet & Duv Special Steel Company purchased a 65000-ton die forging hydraulic press from Ukraine's New Kramato Heavy Machinery Plant (M3) for the production of titanium alloy die forgings and aviation aluminum alloy die forgings.

In 2005, Oberdua, France, and from Sinoil, Germany.CommScopeGroup (Siempe k mp, established in 1883), ordered a 40000-ton die forging hydraulic press. However, due to limited processing capacity, the landing gear titanium alloy components used by European Airbus when manufacturing A380 large passenger aircraft still need to be sent to Russia's 75000-ton die forging machine for processing. The two six-wheel three-axle trolley-type main landing gears of the A380 passenger plane bear more than 590 tons and require a life of 60000 landing gears. Forged of Ti-1023 titanium alloy, it is 4.255 meters long and weighs 3210 kilograms. This is the world's heaviest aviation titanium alloy die forgings.

In the new century, the United States is still making efforts to forge advanced aerospace.

In 2005,American AluminumAcquired the 75000-ton die forging hydraulic press of Russia's Samara Metallurgical Plant, which was the Gubyshev Aluminum Plant before the collapse of the former Soviet Union. In 2001, the California Schultz Steel Plant successfully built a 40000-ton die forging press. However, this is not enough to meet the rapid development of the American aviation industry.

Invest $0.11 billion to refurbish a 45000-ton die forging press built in 1955 at the Cleveland, Ohio plant. In 2015, Weber Metals, located in Los Angeles, USA (WeberMet s) ordered a 60000-ton 540MN drop-down hydraulic die forging machine from the German Symark Group Mel.

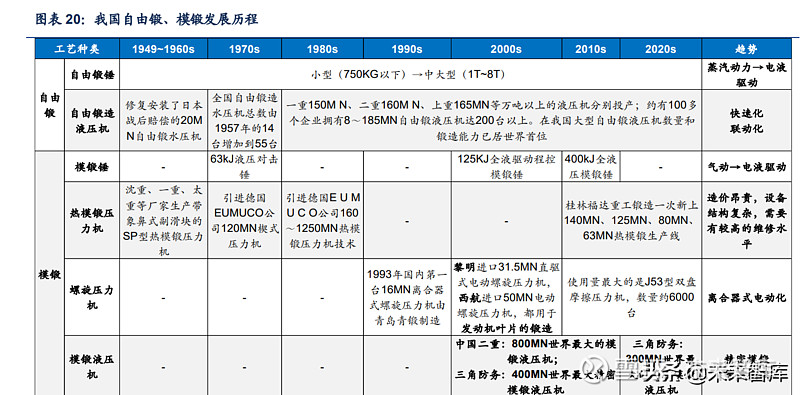

2.2 China's forging industry development positioning high, fast development

China's forging industry started late, and the forging process and equipment manufacturing process have experienced decades of development. From the repair and installation of Japan's post-war 20MN free forging machine, to the current in the field of precision die forging, isothermal die forging to reach the world's leading, after hardships. Since the founding of the People's Republic of China, China's free hammer forging has shown a dynamic transformation from steam power to electric power drive, and the free forging hydraulic press has gradually become fast and linked. Die forging hammer has gradually changed from pneumatic to electro-hydraulic drive, screw press has gradually become clutch-type electric, die forging hydraulic press has been developed by leaps and bounds, creating an international competitive advantage for the development of precision die forging and isothermal die forging.

In 1967, China's First Heavy Machinery Plant built Asia's largest 30000-ton die forging hydraulic press, equipped with Chongqing Southwest Aluminum Processing Plant (112 Factory of the Ministry of Metallurgy). The machine was put into operation in September 1973 and has been in service so far. It has made an important contribution to improving the processing capacity of special high-strength alloy forgings in China, and is known as one of the "four national treasures" of China's industry.

After 40 years of stagnation, we will usher in a new round of rapid development.

Since the first 30000-ton die forging press was put into production in 1973, China has stagnated for nearly 40 years. In 2003, Academician Shi Changxu of the Chinese Academy of Engineering organized a consulting group of "Research on the Development of Large Forging Equipment in China-Construction of 80000-ton Die Forging Hydraulic Press and Its Supporting Equipment" from 31 enterprises and institutions across the country, including five academicians and 17 experts from aviation, machinery, metallurgy, education and other departments, once again, it is suggested to the state that a 80000-ton die forging hydraulic press and a 15000-ton hard-to-deform alloy extruder should be built during the "Eleventh Five-Year Plan" period, so that China can obtain the manufacturing capacity of titanium alloy, high-temperature alloy and ultra-high-strength alloy steel large-scale overall refined die forgings as soon as possible.

On November 15, 2007, the National Development and Reform Commission finally approved China Erzhong Group, in conjunction with Central South University, Yanshan University, Xi'an Heavy Machinery Research Institute and other units, to design and manufacture a 80000-ton die forging press, with a total investment of 1.517 billion yuan, of which the enterprise raised 0.303 billion yuan by itself, applied for a state allocation of 0.4 billion yuan, and applied for a bank loan of 0.8 billion yuan. Planning annual output of aviation, electric power, petrochemical and other titanium aluminum alloy forging 15000 pieces, weighing about 13400 tons.

Around 2010, China explosively developed a number of large presses, with 30000 tons (Kunlun Heavy Industry), 40000 tons (Delta Airlines) and 80000 tons (Deyang Duo) die forging presses each built in 2012 alone.

On March 3, 2012, China's first 40000-ton die forging hydraulic press was thermally tested in Xi 'an Yanliang Triangle Aviation Technology Co., Ltd., and the first large-scale plate products were successfully forged. This machine is currently the world's largest single-cylinder die forging hydraulic press, using steel wire winding prestressed structure. (Source: Future Think Tank)

China's forging equipment ranks among the world's first-class.

In 2013, Deyang Erzhong independently developed the world's largest 80000-ton die forging hydraulic press and put it into production, breaking the 51-year world record maintained by the former Soviet Union in one fell swoop, and realizing the leap of my country's forging products from high-end to the most advanced. The era of foreign countries is completely over. This 80000-ton die forging hydraulic press has a height of 27 meters above ground, 15 meters below ground, a total height of 42 meters and a total weight of 22000 tons of equipment. In 2018, the largest and most complex key bearing forging of the C919 large aircraft, the main landing gear outer cylinder, was localized, which was completed by this 80000-ton die forging hydraulic press.

At present, the world has more than 40000 tons of die forging press countries, only China, the United States, Russia and France. The giant die forging hydraulic press is a national treasure strategic equipment that symbolizes the strength of heavy industry. It is an important symbol to measure a country's industrial strength and military capabilities. There are only a handful of countries in the world that can develop it.

China has advanced technical reserves of die forging hydraulic press. Tsinghua University has developed a 160000-ton die forging hydraulic press, which is more than twice that of Russia's 75000-ton press and more than 3.5 times that of the United States's 45000-ton press.

3. China's forging industry system is complete, rapid development, high barriers

3.1 China has now formed a relatively complete forging industry system

China's forging industry system is more perfect. At present, China's forging industrial system has basically met the needs of domestic economic construction, national defense construction and infrastructure construction. The industry continues to maintain the largest development scale of the forging industry in the world, and has the ability to support the strategic layout of "going out. China's forging industry has now covered aviation, aerospace, navigation, wind power, petrochemical, automotive, medical, heavy equipment and other fields.

The upstream industry of the forging industry is mainly all kinds of metal material smelting enterprises, such as carbon steel, stainless steel, alloy steel, high temperature alloy, titanium alloy, aluminum alloy, etc. The supply capacity and technical level of upstream raw materials directly affect the development level of the forging industry.

The downstream industries of the forging industry are all kinds of equipment manufacturing enterprises with a wide range of applications. Such as aviation, aerospace, shipbuilding, electric power (wind power, nuclear power, hydropower, thermal power), petrochemical, railway and other machinery industries.

China's forging a large number of enterprises, the low-end competition and high-end forging a blue ocean. Most of the forging enterprises are mainly engaged in the production of ordinary carbon steel, alloy steel, stainless steel materials and other forgings. The processing capacity of special alloy materials such as high temperature alloy, titanium alloy, aluminum alloy and magnesium alloy is insufficient, the technical content and added value of the products are relatively low, and the process level is relatively backward.

3.2 China's forging "13th Five-Year Plan" period developed rapidly

The rapid development of China's forging industry during the "13th Five-Year Plan" period benefited from the development of the global economy and technology. The development of the global economy, especially the development of the Internet, digitalization and information technology, has brought about great changes in the pattern of the forging industry; my country's energy-saving and environmental protection requirements are deepening, aerospace, high-end equipment, new energy vehicles, rail transit and other fields Lightweight and efficient development is changing with each passing day, forging raw materials from ordinary steel to high-strength steel, from ferrous metalNonferrous Metalsdevelopment, forging process has made great progress.

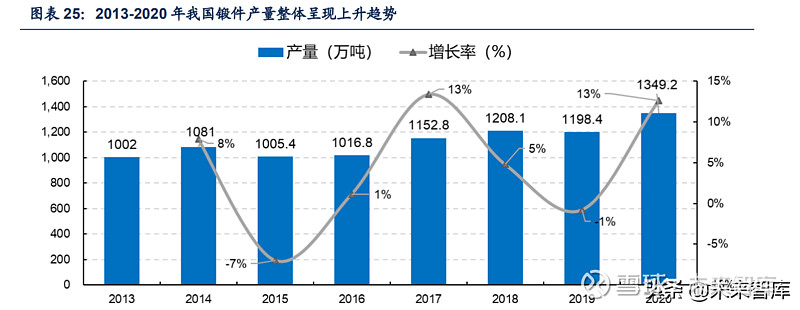

"Thirteen five" period of China's forging production increased year by year. Since 2015, China's forging production as a whole has shown a sustained growth trend, reaching 11.984 million tons in 2019, up 5.04 percent year-on-year, and 13.492 million tons in 2020, up 12.58 percent year-on-year. From the perspective of forging output, China has become the world's first forging power and continues to lead.

During the "13th Five-Year Plan" period, the compound annual growth rate of China's die forging output reached 8.08. China's die forging production growth rate began to decline since 2017, in 2019 China's die forging production declined, and in 2020 die forging production at a growth rate of 14% all the way to 8.85 million tons.

During the "13th Five-Year Plan" period, the compound annual growth rate of China's automobile die forging production reached 6.78. Automobile die forgings are the main products produced in China's die forging industry. From 2017 to 2019, the output of automobile die forgings in China remained consistent with the trend of automobile output, showing a downward trend. It began to rise in 2020 and reached a new high since 2015. In 2020, the output of automobile die forgings was 5.84 million tons, up 19.4 from 4.89 million tons in 2019, accounting for 66.0 of the total output of die forgings.

Compared to 2016 and before, the proportion of automotive die forgings in die forgings has decreased. From 72% in 2016 to 66% in 2020, the corresponding structural space is replaced by high-end die forging of large components such as aviation and aerospace.

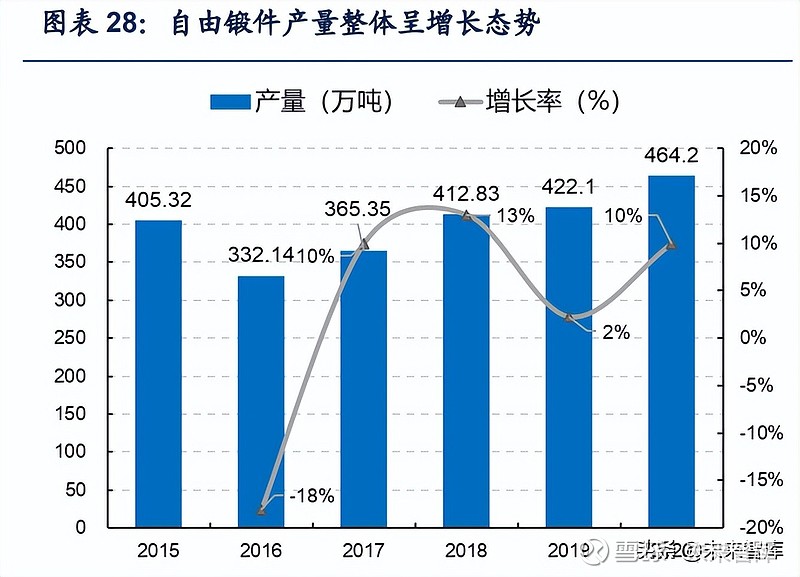

China's free forging production decreased significantly in 2016, with a compound annual growth rate of 8.7 in 2017-2020. In 2020, China's free forging production reached 4.642 million tons, an increase of 10% over 2019.

With the development of national defense industry and aerospace industry, the market demand for ring forgings in China continues to increase, with a compound growth rate of 14.4 from 2017 to 2020. In 2020, 1.247 million tons of production will be achieved, up 62% year-on-year from 2019, accounting for 27% of free forging production. Ring forging is a high-end forging process, mainly used in aviation engines, aerospace equipment, with China's military aircraft and engines, civil aviation engine localization and the rapid development of the aerospace industry, the future of China's ring forging market is expected to speed up development.

China's forging products into the international first-class. Such as civil nuclear power large forgings, large aircraft landing gear, bearing frame, gas turbine disk forgings, fast reactor support ring forgings, nuclear power forging pump shell localization, etc., showing the "13th Five-Year Plan" period forging industry development of the actual level.

Forging equipment large-scale, automation, digital and information fully developed. For example, the number of large electric screw presses, large hot die forging presses, large die forging hydraulic presses, large friction presses, large ring rolling machines and large free forging hydraulic presses is increasing, and the degree of automation of supporting equipment around the production line is obviously increasing.

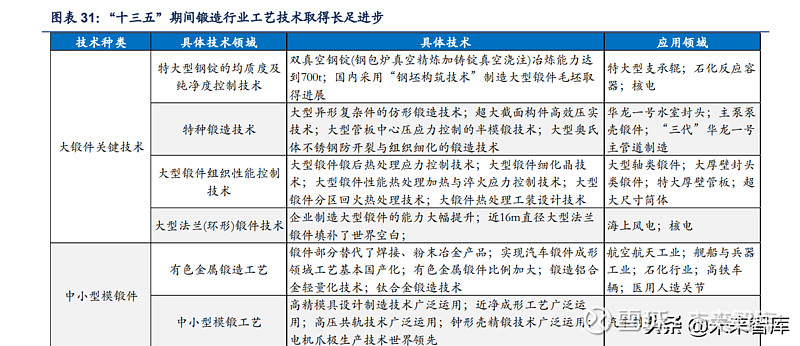

During the "13th Five-Year Plan" period, forging has made great breakthroughs in process technology and equipment technology. In the face of fierce global market competition, the connotation of enterprise management has shifted from the improvement of production capacity to the endogenous power change of improving quality, increasing efficiency and reducing cost. Products, process technology, mold and equipment technology have produced a greater breakthrough. Forging products to achieve diversification, composite, product structure to achieve integration, modular; process technology to achieve material high-strengthening, lightweight, diversification, is to "control", "control", punching and forging combination and other composite process development; mold and equipment technology is moving towards automation, digitization, information in the direction of development.

3.3 policy dividend gives forging industry ultra-high positioning

Based on the basic position of the forging industry in the national economy, since the reform and opening up, the government and industry authorities have given strong support in policy. As the forging industry is in the middle of the industrial chain and is oriented to the high-end equipment manufacturing industry, its upstream high-end material industry and downstream high-end equipment manufacturing industry enjoy a number of national policy support, these policies promote the multi-directional and coordinated development of the whole industry.

In 2006, the State Council issued the "National Medium and Long-term Science and Technology Development Program (2006-2020)", which proposed "developing large-scale and special parts forming and processing technology".

In 2011, the State Council issued the 12th five-year Plan for Industrial Transformation and upgrading, which clearly defined "strengthening the research on basic processes such as casting, forging, welding, heat treatment and surface treatment" and "promoting the innovative development of precision tools and moulds". The National Development and Reform Commission, the Ministry of Science and Technology, the Ministry of Industry and Information Technology, the Ministry of Commerce and the State intellectual property Office jointly issued the "guidelines for key areas of high-tech industrialization that give priority at present (2011). The forging of large-scale construction is listed as a key area of high-tech industry that needs priority development.

In 2015, the China Forging Association issued the "Thirteenth Five-Year Plan for the Development of the Forging Industry", proposing plans for the development of downstream industries such as aero engines and gas turbines, focusing on upgrading basic materials, core basic components (components), advanced basic processes, The "four basics" upgrade plan of the industrial foundation.

In 2016, the General Administration of Quality Supervision, Inspection and Quarantine, the National Standards Committee, and the Ministry of Industry and Information Technology jointly issued the ''Equipment Manufacturing Industry Standardization and Quality Improvement Plan'', emphasizing the research and formulation of basic process standards for metal forming, metal processing, heat treatment, forging, casting, welding, surface engineering, etc. Reliability and life indicators. In the same year, the State Council issued the "Thirteenth Five-Year" National Strategic Emerging Industry Development Plan, which proposed to master the core technologies of processing and manufacturing such as aluminum-lithium alloys and composite materials.

In 2021, the China Forging Association issued the "14th Five-Year Plan for the Development of China's Forging Industry", proposing to focus on the development of basic core technologies, such as basic materials, basic core components, core software, etc., to solve the bottleneck problems restricting the development of the industry, and to enhance the board and make up for the board.

The upstream and downstream policy transmission effect is significant. As a high-end manufacturing process, the forging industry is in the middle reaches of the high-end raw materials and high-end equipment manufacturing industry. Upstream raw material development policies, downstream national defense and military industry, aviation, aerospace, shipbuilding, electric power (wind power, nuclear power, thermal power), petrochemical, automobile and other manufacturing industries are the key high-end manufacturing industries that determine the level of national economic development, and relevant policies recognize and emphasize the foundation and decisive position of the forging industry. The defense industry has introduced policies to encourage private capital to enter the defense industry. With the combination of military and civilian, the military and civilian weapons and equipment research and production system to further promote the construction of forging industry market space to further open up.

3.4 forging industry has high barriers, strong Hengqiang

Forging industry high barriers: market barriers

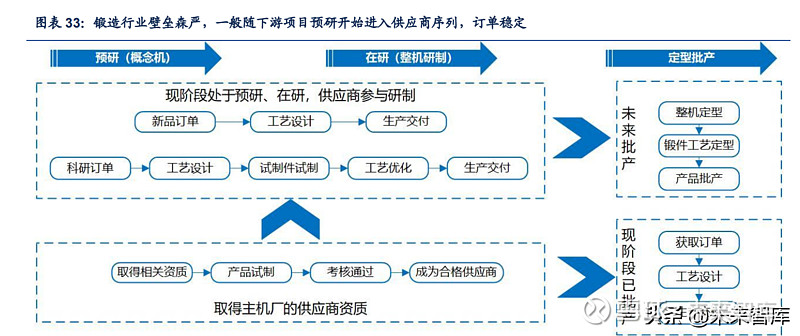

High-end equipment manufacturing industry long-term cycle presents "customized" color, the achievement of forging industry market barriers. Forging products have multi-specification, multi-variety, customized characteristics, the development of the forging industry and downstream customer customization needs are inseparable, therefore, the need to establish a relatively stable partnership with the main customers.

Barriers in the civilian sector lie in entering the downstream host plant qualified supplier directory. On the one hand, before establishing a cooperative relationship with customers, customers have complex assessment procedures for suppliers, long inspection cycles, and specific requirements for product quality, product specifications, supply time, etc.; on the other hand, once the two parties establish a cooperative relationship, The cooperative relationship will generally be relatively stable, and it is difficult for other similar manufacturers to enter.

Barriers in the military industry are affected by technology, model, quality control, stability and many other aspects. The launch of a new equipment needs to go through long-term design, research, test, verification, modification and other procedures of forging product manufacturers, component manufacturers, research institutes, main engine factories, etc., and can be finally finalized after being inspected by the military. At the same time, military customers have extremely high requirements on the quality and technology of products provided by various suppliers. In order to ensure the consistency and stability of products, once the supply relationship of an equipment is confirmed, usually the supply relationship of the equipment will be long-term and stable. As a result, late entrants in the industry will face certain brand and market barriers.

The pre-research mechanism promotes long-term customized upstream and downstream models. The development cycle of aviation equipment is long. In order to ensure the stability and consistency of the product and control the development cycle, the main engine factory usually works closely with the supplier. Generally, the cooperation with the supplier has been carried out for decades since the pre-research of the project. After the project enters the batch production stage, the supplier's sales model will maintain the "order → production" model, usually with an advance payment from the host factory, showing a "customized" color.

Forging enterprises generally focus on one area, while extending to other areas. Different domestic forging enterprises specialize in the main direction of the art industry. SuchTriangle DefensePreference for aerospace forgings, technical preference for die forging and free forging;Aerospace TechnologyThe business scope includes ship forgings, power forgings, aviation forgings, aerospace forgings, petrochemical forgings;Tongyu Heavy IndustryThe main power forgings, including wind power, thermal power and nuclear power.

Forging industry high barriers II: equipment and capital barriers

The construction period of advanced forging equipment is long and the construction cost is high. China has historically relied on imports, and now has the ability to independently develop large-scale die forging hydraulic presses, representing the equipment hasTriangle Defense400MN large die forging hydraulic press, 300MN isothermal die forging hydraulic press. Rolling ring forgings, large free forgings on the equipment requirements are higher, such as forging presses, ring machines and other large equipment, imported equipment unit value is often more than 100 million, the capital requirements are higher.

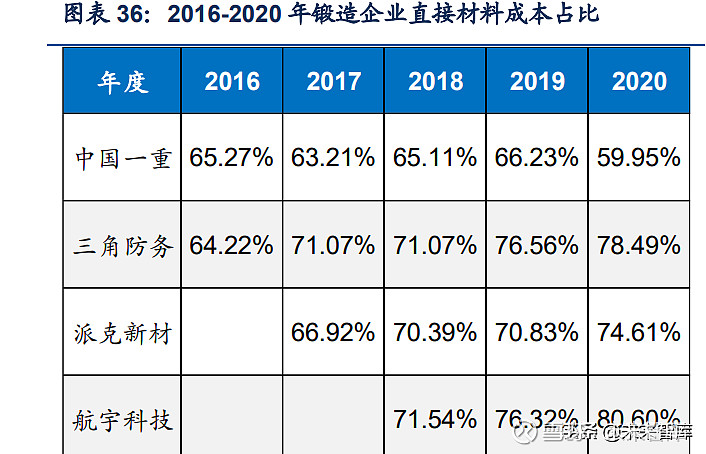

Raw material costs account for a high proportion, and material turnover takes up a lot of money. Raw material procurement and production and operation turnover need to take up a large amount of liquidity, therefore, enterprises involved in the industry must have a strong financial strength or financing capacity, the new entrants to form a high financial barrier. Between 2016 and 2020,Triangle Defense,Parker New Material,Aerospace TechnologyThree forging enterprises direct materials accounted for 70%-80% of the main business costs; and engaged in machining, including forging business.China heavyIts direct material costs also account for about 65% of the main business costs.

Forging industry high barriers three: production technology barriers

Forging industry production technical barriers are high. Forging products have the characteristics of multiple specifications, multiple varieties, and customization. Advanced production equipment, fine quality management, and long-term accumulation of production experience are important guarantees for the long-term development of forging manufacturers. In order to ensure the consistency, stability, reliability and advancement of products, enterprises need a large number of professional R & D personnel and skilled technical staff, and the cultivation of these professional and technical personnel and the mastery of technology need long-term accumulation of enterprises. Therefore, the forging industry has certain production experience and talent barriers.

The raw material must choose the hard deformation material. High performance, long life and high reliability are the eternal goals pursued by the manufacture of high-end equipment forgings in aerospace and other fields to meet extreme service conditions such as high temperature, high pressure, high speed, and alternating load. The use of lightweight, high-strength, high-temperature resistant and other difficult-to-deformation metal materials, such as high-temperature alloys, titanium alloys, aluminum alloys, high-strength steels, etc., is an important way to achieve this goal.

The particularity of materials brings many difficulties to forging. Due to the high alloying degree and complex composition of high-temperature alloys, titanium alloys, aluminum alloys, high-strength steels and other materials, there are many difficulties in actual processing: 1) poor plasticity, easy cracking in the forging process, and strict control of deformation degree; 2) High deformation resistance and poor fluidity require large load equipment; 3) The forging temperature range is narrow, which is easy to produce mixed crystal and uneven structure, increase the number of forging fires and the difficulty of operation; 4) the degree of shape, deformation rate and stress strain state are more sensitive, the forging process is difficult to control; 5) the organization state is complex and diverse, and more sensitive to process conditions, the organization performance is difficult to control.

The forging of hard-to-deform materials is difficult, and there are very strict requirements for the forging process and heat treatment process. The production process must strictly control the process parameters, the formation of a complete control system and control specifications, in order to make the product performance indicators to meet the use requirements. Therefore, forging enterprises to obtain these process parameters and the formation of effective control system, not only need to have a deep knowledge of materials and forging theory, but also need to carry out a lot of repeated calculation and analysis, engineering test verification and long-term engineering practice. Proven and proven production processes are one of the main technical barriers in the industry.

Forging industry high barriers four: military supporting enterprises qualification barriers

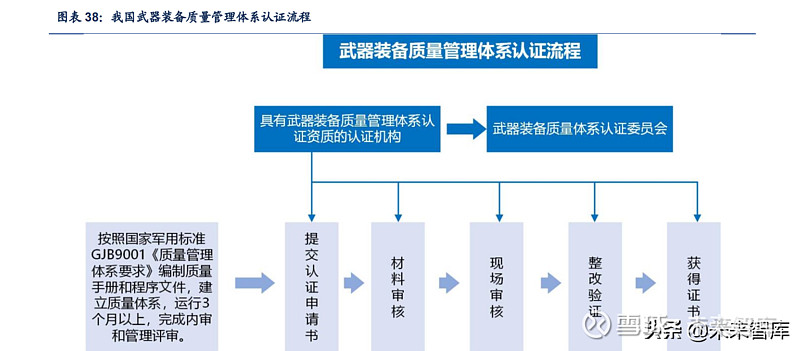

Military supporting enterprises have high qualification requirements, forming a high barrier to new entrants. The state has stricter qualification requirements for private enterprises to participate in the supply of military products, and they need to obtain qualifications such as "Weapon Equipment Research and Production License", "Confidential Qualification Unit Certificate", "Equipment Manufacturing Unit Qualification Certificate", and private enterprises need to go through the military. After a series of comprehensive evaluations on its product performance, quality control, technical level, research and development capabilities, etc. and meet the requirements, only then can we cooperate with military enterprises to provide them with products.

It generally takes a 4-6 year cycle from qualification to performance. Due to the existence of pre-research mechanism in the military industry, forging enterprises need to participate in the whole cycle of equipment development, through a long trial production or small batch production stage, from obtaining qualifications, participation in pre-research to batch production delivery, performance, generally need to go through a cycle of 4-6 years.

4. China's forging industry market is broad, aerospace forging will bring hundreds of billions of market

4.1 China's aviation forging ushered in the best release period, the birth of a hundred billion market.

Aircraft is known as the "flower of industry" and "locomotive of technological development", with a long industrial chain and wide coverage. It plays an important role in maintaining the vitality of the national economy, improving the quality of public life and national security, and promoting the development of related industries.

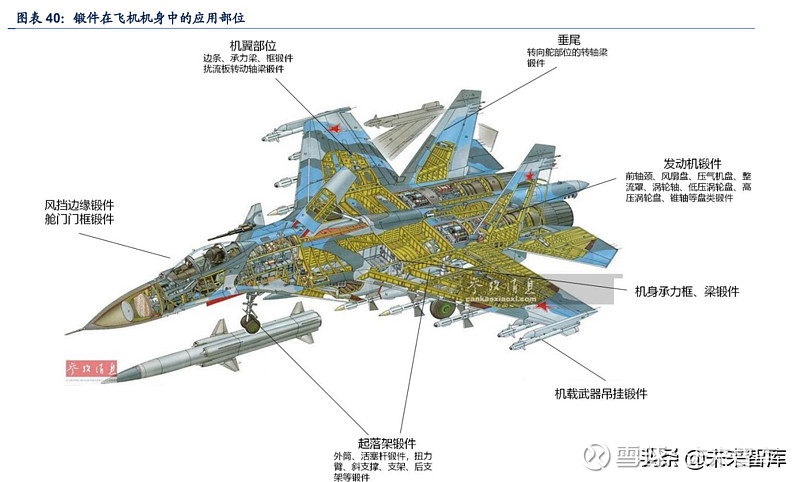

Forgings are the key parts of the aircraft. The weight of the parts made of forgings accounts for about 20% to 35% of the weight of the aircraft body structure and 30% to 45% of the weight of the engine structure. It is one of the important factors that determine the reliability, life and economy of the aircraft and engine. The turbine disk, rear journal (hollow shaft), blades of aero-engine, rib plate, bracket, wing beam, pylon, piston rod and outer cylinder of landing gear are all important forgings related to aircraft safety. Due to the particularity of the materials used in aviation forgings and the working environment of parts, aviation forging has become the industry with the highest technical content and the most stringent quality control requirements. Application in special parts of the equipment can not be replaced.

The forgings in the aircraft fuselage are mainly concentrated on the main structural bearing parts. Including main structural parts such as load-bearing frame, beam frame, landing gear, wing, vertical tail, etc.; windshield, door edge, airborne weapon pylon, etc., which need to bear alternating stress for a long time. The value of aviation engines accounts for about 25% of military aircraft and 22% of civil aircraft.

Li Ding industry research "aircraft body material structure development stage and aviation parts manufacturing value ratio analysis" article pointed out that: military aircraft and civil aircraft because of the use of significant differences, the value of each component of the difference is large. For military aircraft, the power system accounts for the highest value ratio of the whole machine, up to 25%, followed by avionics system, the body structure accounts for about 20%, for civil aircraft, the body structure accounts for more than 13, reaching 36%, followed by power system, avionics and electromechanical systems together account for 30%.

The Securities Guide is published in 《AVIC Heavy Machinery: Gorgeous turn machine manufacturer steel iron bone forging "article pointed out: by value, forgings in aircraft components value accounted for about 6% to 9%, in the aircraft engine value accounted for about 15%-20%.

Aviation forging driver one: military aircraft into the volume production column stage, aviation forging market ushered in a golden period.

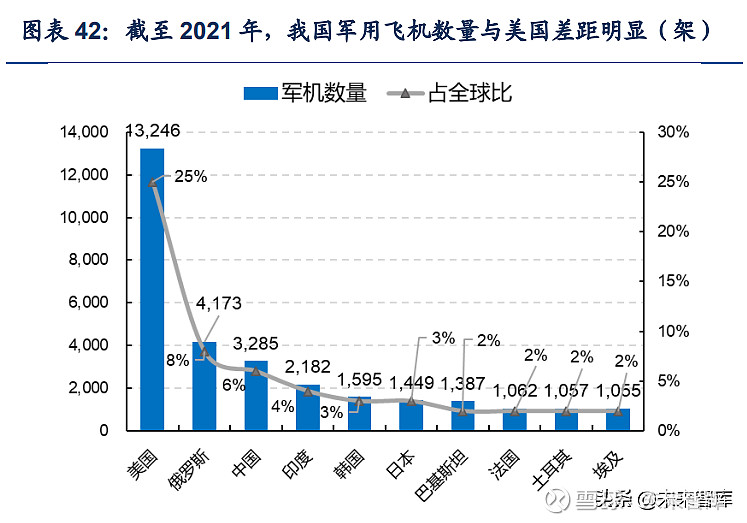

In terms of quantity, there is a large gap between the total number of military aircraft in China and that of the United States and Russia, and there is a lot of room for additional military aircraft. As of 2021, the United States has 13246 military aircraft, accounting for 25%, ranking first in the world; followed by Russia, with 4173 aircraft, accounting for 8%. China has 3285 military aircraft, accounting for 6%. In horizontal comparison with the United States and Russia, the total number of Chinese military aircraft accounted for 24.80 per cent and 78.72 per cent respectively. In the future, in order to cope with the increasingly fierce international competition, there is a lot of room for military aircraft to be supplemented.

From the intergenerational point of view, China's military aircraft are in urgent need of iterative upgrade. Both the United States and Russia have eliminated second-generation fighters and completed the transformation to third-and fourth-generation fighters. China is currently in the process of phasing out the second-generation machine and transforming to the third-generation machine, and there are still a large number of second-generation machines in service.

As the heart of the aircraft, the aero-engine has ultra-high requirements for materials and has become a new growth pole for aviation forging.

Aero-engines have high requirements for manufacturing processes. The pursuit of high-performance aero engines is to ensure long-term stable service performance under extremely limited weight and working space, and extremely harsh working conditions. Its manufacturing technology requirements are extremely high, which is an extreme manufacturing situation.

Lightweight structure, hard-to-deform raw materials and thin-walled parts with complex profile put forward high requirements for aero-engine manufacturing process. In order to achieve high thrust-to-weight ratio performance requirements, aero-engines adopt a large number of complex overall lightweight structures, such as hollow blades, wide chord blades, integral bladed discs, etc., to achieve maximum weight reduction. At the same time, high-performance titanium alloys, high-temperature alloys and composite materials are also widely used, and these materials are typical difficult-to-process materials. In addition, the heavy parts of aero-engines are mostly thin-walled parts with complex profiles, the requirements for machining accuracy and surface quality are extremely high.

Precision forging is essential in aero-engine manufacturing. Jia Li and others pointed out in the article "Precision Manufacturing Technology of Aero Engine Parts": At present, the blank of aero engine parts and forgings accounts for more than 50% of the total weight of the blank, and precision forging technology has gained attention and is widely used in aero engine manufacturing enterprises. The blank of engine parts manufactured by precision forging technology has a precise blank shape, which can realize the processing and manufacturing of hollow turbine blades, integral turbines and other parts with small cutting allowance or even no cutting allowance. With the development and application of advanced forging technology such as isothermal die forging and superplastic isothermal die forging, aero-engine manufacturers have been able to manufacture non-segregation ultra-fine grain blanks and mass-produce non-margin precision forging blades.

Aero-engine ring forgings mainly include aero-engine ring forgings and aero-engine casing. Among them, the aero-engine ring forgings include other ring forgings except the casing, mainly including sealing ring, support ring, fan flange ring, fixed ring, compressor interstage retaining ring, combustion chamber nozzle outer wall ring, turbine guide ring, rectifier ring, etc. The casing includes fan casing, compressor casing, combustion outdoor casing, high pressure turbine casing, low pressure turbine casing, etc.

Forgings have a central position in aero-engines. The article "Analysis Report on Market Prospect and Investment Strategic Planning of China's Aero Engine Industry from 2013 to 2017" released by the Prospective Industry Research Institute analyzes the value proportion of various parts in military aircraft aero engines. Among them, the disc shaft, blades, frames, casings, combustion chambers, transmission devices, etc. that use a large number of forgings account for more than 70% of the total engine value. Thus, forgings play a core role in aero engines.

The engine is an expendable item and will be refurbished approximately 4 times during its life cycle. Its performance and fuel consumption are related to the number of renovations, and the number of aero-engine renovations affects the cost of renovations.

The attenuation of thrust and the increase of fuel consumption are the main reasons for the engine renovation. Aeroengine renovation has caused the components of the aero engine to be in a high temperature and high pressure working environment for a long time. As the use time increases, some parts will fail due to fatigue cracking, and the performance of the engine will also be reduced, and the fuel consumption of the engine will also increase. During the service life, the performance attenuation of the engine shall meet the relevant requirements of the GJB241A-2010 General Specification for Aviation Turbojet and Turbofan Engines, the thrust attenuation shall not exceed 5%, and the increase in fuel consumption shall not exceed 5%. When the engine performance decreases to this red line, it should be returned to the factory for repair. Generally, the engine performance can be restored by repair.

Engine refurbishment can restore performance, but the more refurbishment, the more limited the reliability recovery. In the first renovation period, there are many early failures and the mean time to failure (MTBF) is short. In each renovation period, the reliability is restored after the overhaul (MTBF increases), but MTBF gradually decreases with the increase of service time. In the whole life cycle, the interval time of each overhaul is gradually shortened, the overhaul is gradually frequent, and the MTBF is gradually shortened after each overhaul.

Aero engines can generally be refurbished up to four times. Dong Honglian and others described the test to study the relationship between engine performance, fuel consumption and the number of renovations in the article "Aviation Engine Life Control System and Life Assessment Method. The performance re-inspection of 35 engines with different repair times was carried out, and it was found that with the increase of repair times, the engine performance decay rate gradually accelerated, and it was predicted that the performance and fuel consumption of the engine did not meet the requirements of GJB 241-2020 when the engine was used for the fifth overhaul. That is, the engine can only be overhauled a maximum of 4 times in the whole life cycle. In the actual operation of aero-engines, more reference should be made to the economic problems brought about by the increase in renovation costs. In principle, the cost of engine overhaul should not exceed 50% of the purchase cost of new aircraft.

The replacement rate of overhauls increases gradually with the number of overhauls, which is 9.8 per cent for the first overhaul, 11.91 per cent for the second overhaul, 12.38 per cent for the third overhaul and 14.74 per cent for the fourth overhaul. Replacement rate and test run pass rate are important indicators for evaluating repair damage and repair economy. Forging parts such as engine discs, shafts, blades, and casings are important parts that affect safe use and are of high value. According to the existing air force duty and training plan, assuming that China's military aircraft fly 240-300 hours per year on average, the flight time of fighter aircraft is calculated in 240 hours per year, and the flight time of other aircraft types is estimated in 120 hours, the calendar life of aero-engines can be estimated. (Source: Future Think Tank)

Aviation forging driver two: domestic large aircraft traction civil aircraft parts forging industry to take off.

As of the end of 2020, the number of civil aviation industry-wide transport aircraft at the end of the period was 3903, of which: 3717 passenger aircraft, respectively, 458 wide-body, 3058 narrow-body, 201 regional; 186 cargo aircraft. Up to now, China's self-developed 90-seat regional passenger aircraft, ARJ21-700, has delivered 66 aircraft. Orders for the 190-seat trunk passenger plane C919 have reached 815. The 280-seat long-range trunk passenger plane CR929 has completed the G3 phase of project development.

According to the forecast of China's average annual GDP growth rate, the average annual growth rate of passenger turnover in China is 5.7 percent, and the average annual growth rate of aircraft fleet is 5.2 percent. In the next two decades, the Chinese aviation market will receive 9,084 passenger aircraft of 50 or more seats, worth about US $1.4 trillion (based on the 2020 list price). Among them, there are 953 turbofan regional airliners with 50 seats or above, 6,295 single-aisle jetliners with 120 seats or above, and 1,836 dual-aisle jetliners with 250 seats or above. By 2040, China's fleet size will reach 9,957 aircraft, accounting for 22% of the global passenger aircraft fleet, becoming the world's largest single aviation market.

The life of civil aviation engines is generally longer than that of military aviation engines. There are generally two ways to measure civil aviation, one is the number of engine cycles, and the other is the engine hour life. In this paper, the hourly life of the engine is used as the basis for calculation. In the future, narrow-body trunk airliners will be the main force of aircraft growth. The first renovation interval of a new generation of aero-engines can reach 15,000-20,000 hours, which is much longer than that of military aero-engines. However, mainstream airlines, such as Air China, China Eastern Airlines and China Southern Airlines, have a daily utilization rate of about 10 hours, with an average of about 3650 hours per aircraft per year. Based on this, we estimate that the calendar overhaul interval for civil aviation engines is 4.11-5.48 years, and the general overhaul interval for aviation OEMs is 5 years.

Aviation forging driver three: China's civil aviation subcontracting business into a period of rapid development, is to the first echelon of the rise.

Aviation "subcontracting" production is a supply chain cooperation model based on "main manufacturer-supplier" commonly adopted by global aviation aircraft and engine manufacturers. The subcontracting of the international aviation industry is roughly divided into three echelons. my country is still in the second echelon and is rising to the first echelon.

China's aviation industry foreign trade subcontract production began in 1980, has with the United StatesBoeingAirbus Europe, Bombardier Canada,Brazilian Aviation IndustrySuch as the world's advanced aircraft manufacturing companies and engine manufacturing companies such as GE Company of the United States, Rolls-Roo Company of the United Kingdom and Pratt & Whitney Company of the United States have developed industrial cooperation relations and carried out extensive foreign trade subcontracting production of aviation parts. The project involves a variety of products such as nose, wing, fuselage, tail section, hatch, engine ring forgings, casing, blades, etc. At present, China's aviation subcontracting business is in a period of rapid development.

The subcontracting business of the international aviation industry is roughly divided into three echelons, and China is in the second echelon, mainly for the manufacture of airframe structural parts and aviation parts, and the assembly of components. The first echelon is mainly for design and development, engineering manufacturing and integration of large components, with complex technical difficulties and high added value. The participants are represented by the United States, Europe and Japan. The second echelon is mainly for the manufacture of airframe structural parts, the manufacture of aviation parts and the assembly of parts. The technical difficulty and added value are in the middle. The participants are represented by China, South Korea, Mexico and Tunisia. The third echelon is mainly for the supply of parts and components, with low technical difficulty and added value, participants were represented by Russia, India and Malaysia.

China's aviation industry foreign trade subcontracting is rising to the first echelon. With the establishment of Airbus (Tianjin) General assembly Co., Ltd. in 2017 and 2018Boeing(Zhoushan) With the completion of the delivery center, China's aviation industry's foreign trade subcontracting has officially sounded the clarion call to be promoted to the world's first echelon, and has begun to move from parts subcontracting to a new level of final assembly and delivery.

China's aviation industry subcontract business delivery amount increased year by year. According to the 2020 of China Civil Aviation Industry Yearbook, the subcontracted production and delivery amount of China's civil aviation products in 2019 was 2.56 billion billion US dollars, an increase of 40.5 percent over the same period last year, of which aircraft parts were 1.44 billion US dollars, an increase of 36.0 percent over the same period last year; engine parts were 0.7 billion US dollars, an increase of 2.5 percent over the same period last year; civil aviation airborne systems and equipment parts were 0.1 billion US dollars, an increase of 11.2 times, year-on-year growth of 3.4 times. New orders for subcontracted production were $2.23 billion, up 1.1 percent year-on-year, while reserve orders were $4.68 billion, down 13.5 percent year-on-year.

AVIC and AVIC are the main players in the international subcontracting business of aviation, with extensive participation of private enterprises and rapid development momentum, and the relevant participants have obtained the qualification of qualified suppliers of international aviation/aviation giants.

The subcontracting of airframe structural parts focuses on the production of airframe structural parts and components. The mode of participation has gradually evolved from subcontracting production of parts to centralized delivery of components and large sections. The completion of Airbus (Tianjin) final assembly base has pushed China's subcontracting of aviation projects to the final assembly. The participating manufacturers include XAC, Shenfei, Chengfei, Hafei, Changfei, Hongdu and Shangfei, which is a subsidiary of Comac.

The aero-engine subcontracting business focuses on the manufacture of shafts, rings, casings and blades. The participating manufacturers are mainly Liyang and Liming, which are owned by China Aviation Development,AVIC Heavy MachineryHongyuan, Anda, and private enterprisesAerospace TechnologyWait.

Aviation subcontractors have obtained the relevant qualifications of international aviation giants. The airframe business participants have acquiredBoeingQualified supplier qualifications for aircraft manufacturers such as Airbus, Embryos, Bombardier, etc.; subcontracting participants in the aviation business includeAVIC Heavy MachineryAnda Forging, Hongyuan Forging,Aerospace Technology,Parker New MaterialThe relevant participating manufacturers have obtained, in whole or in part, GE, Rolls-Roads, Safran, Megatt, Pratt & Whitney, Collins, and,HoneywellQualified supplier qualifications for aviation giants such as MTU.

Technology "internal work" to enhance the reduction of "external demand" to expand, the future aviation forging subcontracting business will be more "new level".

The improvement of China's aviation forging technology and process level has driven the transfer of international aviation subcontracting business to China. With the emergence of Chinese aviation parts manufacturers, the production process and technical level continue to improve, and the product quality and stability can meet the high quality requirements of international aviation engine manufacturers.

The need to reduce costs has pushed international aviation giants to expand the outsourcing of aviation forging business in China. In order to reduce costs and improve profitability, the international aviation parts subcontracting business will continue to transfer to China, bringing more development opportunities for China's aviation forging, aviation ring forging research and development, production enterprises.

4.2 satellite launches stimulate the demand for aerospace forgings for launch vehicles

The aerospace industry is a national strategic industry and an important guarantee for safeguarding national sovereignty, territorial integrity and political security. The level of space equipment is not only the core symbol of a country's space capability, but also one of the important symbols to measure the country's comprehensive national strength. After decades of hard work since the founding of the People's Republic of China, my country's aerospace industry has gradually developed from the initial simple imitation to the current self-developed, and is developing in the direction of low-cost, rapid response manufacturing, and has achieved a considerable number of key process technologies in some fields. Some of the breakthroughs are close to the international advanced level. The aerospace industry is one of the few advanced industries in my country that can compete with developed countries in the international market.

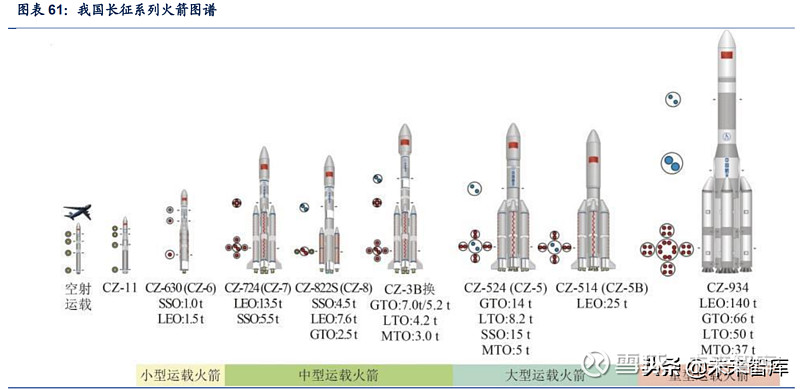

The launch vehicle isspace developmentKey equipment. As a carrier that pushes satellites, spacecraft, space stations, and deep space probes into predetermined orbits, the development of launch vehicles is closely related to the development of the latter. In order to ensure major aerospace projects such as my country's satellites, space stations, manned spaceflight and lunar exploration projects The development of my country's launch vehicles is also very rapid. Up to now, the "Long March" series of carrier rockets with independent intellectual property rights and strong international competitiveness have become the main force of my country's carrier rockets. The Long March series of carrier rockets have the ability to launch low, medium and high satellites in different orbits and different types. As of 2021 On December 30, my country's Long March series of carrier rockets have been launched 405 times.

At present, China's main launch vehicle is the Long March series of rockets, and its technological development started in the 1950 s. With the strong support of the state and the unremitting efforts of several generations of astronauts, 15 models of Long March series carrier rockets, including Long March 1, Long March 2, Long March 3, and Long March 4, have been developed, and they have initially possessed a relatively complete range. Carrying capacity. It has realized the leap-forward development from normal temperature propellant to low temperature propellant, from series to bundling, from one arrow single star to multiple stars, from launching satellites to launching manned spacecraft, from launching earth orbit satellites to launching deep space probes. It has the ability to send spacecraft into any space orbit, occupies a place in the international satellite launch service market, and has constructed a long March series of launch vehicle spectrum with independent intellectual property rights in China.

The number of launch vehicles in our country is rising. Since 2018, the number of orbital launches of China's launch vehicles has been the first in the world for a long time, especially in 2021, the number of launch vehicles in China has shown a blowout growth. As of December 30, 2021, China had launched rockets 55 times, 10 times more than the United States, an increase of 41% over the whole of 2020, and the number of launches accounted for 38% of the global number of launches.

Author: Future Think Tank

Link: https://xueqiu.com/9508834377/215891971

Copyright is owned by the author.

Related News

Address: Building 88, Capital Airport International Center, No.6 Changcheng South Road, Qingdao

Xia Feng:+8613853229526

E-mail:xiafeng@qdhczn.com

An Wenyang:+8613869862964

E-mail:anwenyang@qdhczn.com

Concerned about the public.

Pay attention to the tremolo

©2023 Qingdao Huchuang Intelligent Equipment Co., Ltd. Powered By 300.CN SEO Tags city substation Business License

{kind=link}